When a home appraises below the agreed purchase price, frustration usually follows.

Buyers worry about financing.

Sellers question the valuation.

Agents scramble to save the deal.

But the reality is that appraisals are often misunderstood. Many people assume an appraisal is simply a confirmation of the contract price. In reality, appraisers evaluate a property through a much more detailed process designed to determine market value based on evidence, not emotion.

In this conversation, professional appraiser Anthony Young joins Beatrix Whipple to explain what truly drives appraised value and why understanding the process can help buyers, sellers, and homeowners make better decisions.

Why Appraised Value Matters

Most people focus on price.

Appraisers focus on value.

While those two numbers are often similar, they are not always the same thing. Price reflects what one buyer agreed to pay. Value reflects what the broader market would likely pay under normal conditions.

That distinction becomes especially important when lenders are involved because loan approval depends heavily on the appraised value of the property.

The Problem with Price Per Square Foot

One of the biggest misconceptions in real estate is the idea that price per square foot can accurately determine a home's value.

According to Anthony Young, price per square foot is useful as a directional tool, but it should never be treated as a calculator.

Larger homes generally sell for a lower price per square foot than smaller homes because of economies of scale. Factors such as lot size, condition, quality of construction, location, and usability all influence value in ways that simple square footage calculations cannot capture.

Price per square foot can become more useful when comparing highly similar properties with nearly identical characteristics, but even then, it should only be one piece of the analysis.

How Appraisers Really Determine Value

Appraisers are not trying to justify a contract price.

They are trying to answer a different question:

What would this property likely sell for in today's market?

To answer that question, appraisers analyze:

- Comparable sales

- Property size and layout

- Lot characteristics

- Condition and quality

- Location and neighborhood influences

- Market trends

- Recent buyer behavior

The goal is to determine how the property competes against other available options in the marketplace.

Why Multiple Offers Matter

One topic discussed in depth was whether competing offers help support value.

The answer is yes, but only when properly documented.

If several buyers independently arrive at similar offer prices, that information can help demonstrate market acceptance of a particular value range. However, appraisers still need supporting market evidence through comparable sales and other data.

This is why experienced agents often provide appraisers with detailed packets containing:

- Comparable sales

- Market condition reports

- Upgrade lists

- Multiple offer information

- Neighborhood insights

The goal is not to influence the appraisal but to provide objective information that may help the appraiser fully understand the property and market.

The Most Overlooked Factor: Market Movement

According to Anthony, one of the most important skills in valuation is understanding how the market has changed over time.

A comparable sale from four months ago may not reflect today's market conditions.

If prices have risen, adjustments may be necessary.

If the market has softened, those same adjustments may move in the opposite direction.

Without accounting for market movement, even strong comparable sales can lead to inaccurate conclusions.

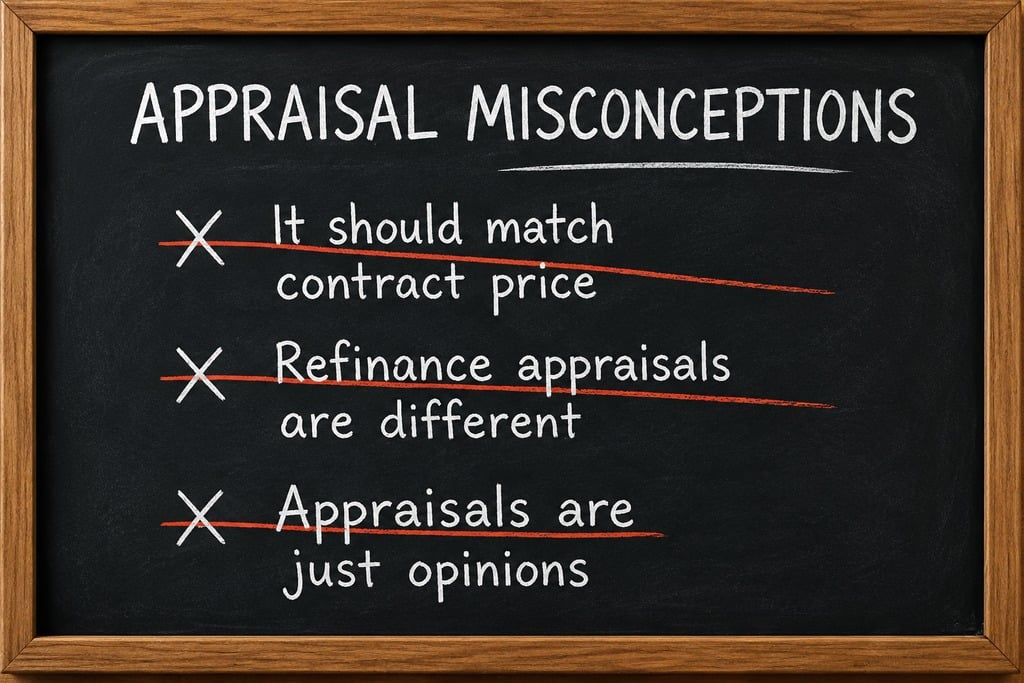

Common Appraisal Misconceptions

One misconception is that appraisals for refinances are different from appraisals for purchases.

In reality, the valuation process is largely the same. Appraisers are determining market value as of a specific date, regardless of the reason for the appraisal.

Another misconception is that an appraisal should automatically match the contract price.

While contract price is important information, appraisers must still support that value through market evidence.

Why Some Homes Appraise Below Contract Price

A low appraisal often happens when one or more of the following occur:

- Comparable sales do not support the agreed price

- The market has shifted since earlier sales occurred

- Buyers paid a premium beyond what the broader market supports

- Unique property features are difficult to measure with available data

- Sellers relied on outdated market expectations

A low appraisal does not necessarily mean the property is undesirable. It simply means the evidence available at that moment does not fully support the contract price.

The Human Side of Appraisals

Despite all the spreadsheets, statistics, and reports, both Beatrix and Anthony repeatedly return to the same point: real estate is ultimately about people.

Every appraisal affects someone's future.

A family buying their first home.

A seller moving to the next chapter of life.

An investor making a significant financial decision.

While data drives the valuation process, the outcome impacts real people and real lives.

Final Thoughts

If your appraisal comes in lower than expected, it does not automatically mean something went wrong.

More often, it means the market is communicating information that buyers, sellers, and agents need to understand.

The strongest pricing strategies are built on more than optimism. They combine market data, neighborhood knowledge, comparable sales, and an honest understanding of current conditions.

When everyone approaches the process with accurate information and realistic expectations, appraisals become less of a surprise and more of a valuable tool for making informed real estate decisions.

Check out this article next